Transitioning from working life to retirement can be an exhausting and nerve racking time. With so many aspects to consider many people become overwhelmed and constantly struggle with that dreaded feeling of having forgotten something.

As you get older your financial mind tends to shift from aspects of raising your family and enjoying your working life to preparing for your retirement. At Wakefield Partners we believe that in regards to your finances, the earlier you start preparing for your retirement, the better off you will be.

Our life expectancies are increasing over time. We are living on average seven years longer than we did in 1980 and this trend is rapidly increasing. The problem is that as we live for a longer period of time we also need to support ourselves for longer in retirement. This is compounded by the fact that, as a general trend, we are retiring earlier these days.

It is up to each individual to plan sensibly so the chance of having sufficient assets to fund their lifestyle throughout retirement is maximised.

The three main sources of income in retirement come from:

- Superannuation – in the form of a pension income stream and/or lump sum withdrawals

- Non Superannuation Assets – in the form of returns from personal investments

- Centrelink Age Pension

The capital required to provide the income from these sources (excluding Centrelink) will vary depending on how much you plan to spend in retirement, your age at retirement and how long you need the funds to last.

The following table demonstrates various income levels and the estimated capital that would be required given the number of years spent in retirement.

| Income Needed in Retirement (pa) | 20 Years in Retirement | 25 Years in Retirement | 30 Years in Retirement |

| $30,000 | $420,000 | $484,000 | $536,000 |

| $40,000 | $560,000 | $645,000 | $715,000 |

| $50,000 | $700,000 | $806,000 | $894,000 |

| $60,000 | $840,000 | $967,000 | $1073,000 |

| $70,000 | $980,000 | $1,128,000 | $1,251,000 |

Source: SPAA Annual Conference 2007. Assumptions: 7%pa return. 3%pa inflation, tax & fees not included.

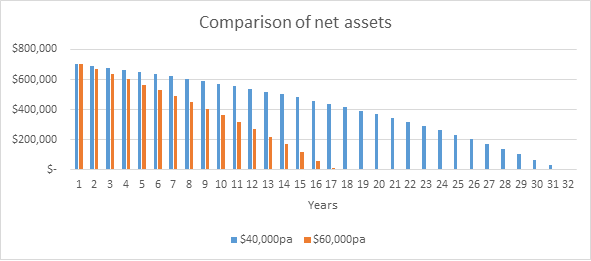

How long you continue to derive income from your saved capital will obviously depend on how much you spend each year. The chart below shows the capital outcome if an individual draws an income of $40,000 pa vs drawing an income of $60,000 pa, based on a starting capital amount of $700,000.

Source: Wakefield Partners estimation. Assumptions: 4%pa return, tax & fees not included.

As you can see the difference in how long capital lasts is quite significant. For this reason, careful planning for your retirement is crucial. At Wakefield Partners we specialise in assisting clients to financially prepare for survive retirement. We not only assist with the management of your Super and Non Super Investments but we can also help to ensure that you receive any possible Centrelink benefits available to you.

Centrelink is there to supplement other income if your financial position qualifies you for a full or part Age Pension payment. However, there should not be a heavy reliance on this as there are concerns about continued affordability of Government benefits. Lower birthrates and increasing life expectancies are resulting in the average age of the population above retirement age to increase. The implication of this is that it places increasing pressure on the Government to fund.

You can see why being self-funded or largely self-funded in retirement is very important. The more you have saved in your super and non-super portfolios means a more comfortable standard of living in retirement – without relying on Government handouts.

So how can you best plan to have sufficient assets to fund your lifestyle in retirement? The answer; Strategic Planning.

Strategic planning is an integral part of retirement planning. It is the process of determining where you are now and where you would like to be during your retirement. It involves analysing your current situation and setting goals, then designing a strategy to achieve those goals.

The process is relatively straight forward but needs to be conducted in a structured way. This is where an experienced planner can help. At Wakefield Partners we can help you detail your goals and document a clearly defined strategy to help you achieve them. We want you to tell us your objectives and priorities, it’s your life, and it’s your money. Our role is to purely advise you how you can achieve these goals, and help you implement recommendations that are appropriate for you.

For retirement planning advice, we generally offer an introductory appointment free of charge. This appointment will generally take up to one hour and our adviser will then be able to provide an indication of what further action is recommended. The initial appointment is without obligation and provides potential clients with the opportunity to meet us and discuss their situation.