The Federal Budget was released on Tuesday night the 6th of October 2020 – delayed from May due to the ongoing coronavirus pandemic. Many Australians may benefit from the tax cuts that have been brought forward from 2022.

The tax rates will now be as follows:

| Income Range | Tax Rates |

| Up to $18,200 | 0% |

| $18,201-$45,000 | $0 + 19% over $18,200 |

| $45,501-$120,000 | $5,092 + 32.5% over $45,000 |

| $120,001-$180,000 | $29,467 + 37% over $120,000 |

| $180,001+ | $51,667 + 45% over $180,000 |

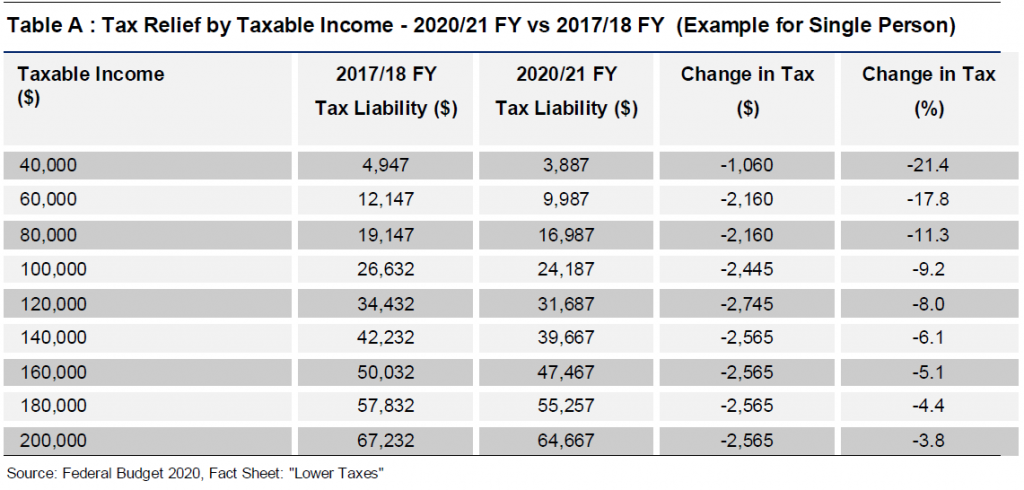

But what does this mean in real terms??? The Government have released the below table to give an example of how the tax savings might look to an individual.

The column that should most be noted is the ‘Change in Tax $’ column. An example of the benefits of this tax cut is the Administration Assistant who earns $80,000 per annum, she will be $2,160 better off through the process of being taxed less throughout the year. On the other hand, the coffee shop attendant earning $40,000 per annum will be $1,060 better off for the same year.

There are also some Low Income Tax Offsets that may assist with boosting your income at tax time. These will be applied automatically to your tax return when you lodge it.

Now that we are aware of the extra funds that we will have, what should we do with it??

- Save It

- Spend It

- Contribute to your superannuation

- Pay down debt

- Start a share portfolio

1. Save It

Maybe the pandemic has shown you that circumstances can change quickly and that you aren’t prepared should negative events impact you in the future. Having a savings account with a portion of your yearly income is helpful to have when you may need it urgently. The car breaking down, an insurance claim excess payment, or a medical event that requires funds sooner rather than later can all be reasons why having some money set aside is a brilliant idea.

2. Spend it

In the same vain as the stimulus packages that were offered earlier in the year, the tax cuts are being executed to stimulate the economy. This means giving the public excess funds to spend at retailers, food and drink establishments and the like to increase the need for jobs. Unemployment is quite high at the moment with many still unable to work. So on that note, spend your dollars to assist getting Australia back out of the recession and boost the employment rate!

3. Contribute to your Superannuation

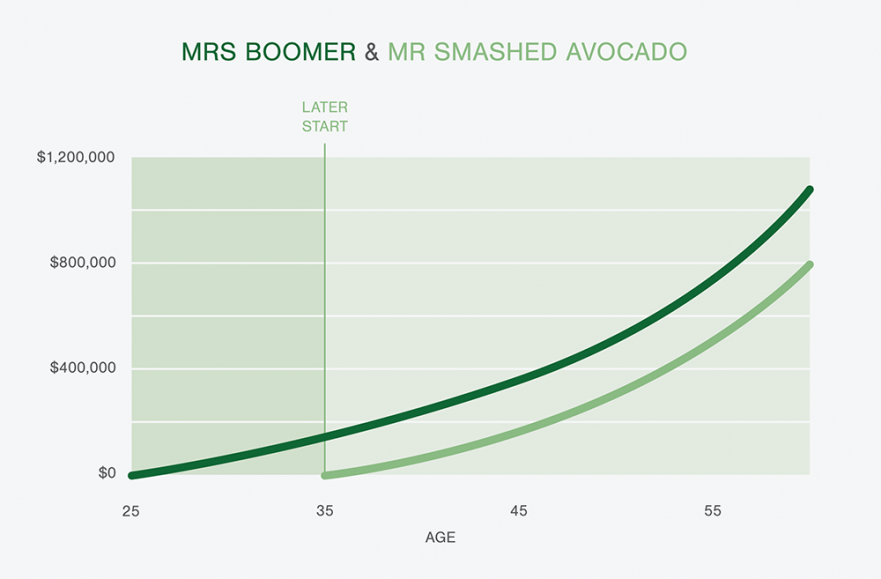

Perhaps you would like to start a regular contribution plan into your superannuation. Putting a small amount each week into your super can have larger compounding effects down the track, read our article on compounding here. A further benefit of contributing to your superannuation is the lowering of your tax liability again. For instance, if you earned $80,000 and contributed $2,000 pa (or just under $40 per week) into your super, you assessed income at tax time would be $78,000, leading to a reduced tax bill.

4. Pay down debt

Have you got yourself in a bind with bills or loans that you’re struggling to pay off? Paying these liabilities down will give you a great sense of relief and satisfaction! With credit card debt being a worry for many Australians coupled with the interest rate of approximately 20%, paying off debt makes sense. Choosing between paying off a credit card or putting more money on your mortgage? Perhaps choosing the option that causes you to lose sleep at night or (financially speaking) the option with the highest interest rate, is the best decision for you and your family.

5. Start a Share Portfolio

Is this your opportunity to enter the market with excess funds you didn’t know you would have? The current economic climate has caused many holdings to trade at a discount, giving the perfect opportunity to invest in some special interest companies, or the blue chip shares that you have heard about time and time again. You can begin investing with $500 and still gain broad exposure to the market should you wish. Speak to us today for some ideas on investing in the share market!

There are many other things you could do with your excess funds but we hope that this has given food for thought and you have perhaps made some goals for yourself to assist in rebuilding after a pandemic and recession. We are here if you want to discuss any fears you may have or if you would like help understanding the budget specifics. Contact our advisers today!