It was announced by the Federal Government on the 22nd of March 2020 that the income stream minimum requirements have been halved. What does this mean for you?

If you are accessing your superannuation via an account based pension, you now have some options. If you are taking more than you need, because of the Government-enforced minimum percentages, you can make a change. If you are worried about the value of your assets, you’ve got some thinking to do. For those who have set their regular pension payments at the amount they actually need to live, this probably doesn’t impact you.

For those who received allocated pension payments during the GFC, they will remember the Government of the day did exactly the same thing. The main aim is to prevent pensioners selling down assets at absolutely the worst time to fund pension payments. For our clients, we typically maintain 12 month’s worth of pension payments in cash at any time, meaning that selling down of assets is often unnecessary, however this is not the case for all pension funds.

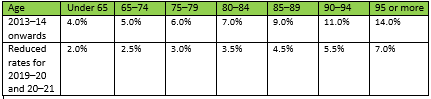

For those who are interested in the numbers, the figures are in the below table.

It can probably be best explained by an example:

Take George (Age 85) and Mildred (Age 81). They both have account-based pensions. George was taking the minimum payment of 9% per annum of his balance. Under the new rules, his requirement is now only 4.5% of his balance. For the remainder of this financial year (2019/20), he may choose to stop his payments altogether, reduce them or leave them as they are. Mildred has previously chosen to draw down $2,000 per fortnight ($52,000 pa) which is well above her 7% minimum requirement. She may choose to continue her regular payment, reduce or cease the payments as was the case with George. Next financial year, they will both be presented with options to take the new minimum.

George and Mildred are not required to make any changes if they don’t want to. They may still require the same payments as before. This is the same for all pensioners receiving an income stream.

There are some important things to consider with these changes:

- Once funds have been withdrawn from an account-based pension, it cannot (in most cases) be contributed back. If you want to reduce the payments, act as soon as possible.

- Pension providers seem to be a little slow in making these options available to clients. accounts. If you want to make changes, you may need to take the lead.

- For those taking income streams from Self Managed Super Funds (SMSFs), seek advice regarding the options available to you.

So what should you do? Each individual’s circumstances are different. If you want to reduce your ongoing payments and can live comfortably in doing so, then seemingly it makes sense in these volatile times. If you still require the amounts you were drawing down before, then perhaps you should continue as is. These are difficult times, and require rational decision making.

Need help deciding what you should do in regards to the reduced pension minimums announcement? Some fund managers have implemented these changes automatically. Please contact the team at Wakefield Partners today to discuss your needs or if you are unsure of your fund managers’ decisions.