Writing these quarterly articles, I was glad when the worst of COVID was finished. I could only spin how the pandemic impacted your investments so many ways, and it felt good to move on! That said, the new theme of inflation is proving just as stubborn.

It’s been the only game in town now for the last 12 months! Rather than rehash what is causing it (I did that a few months ago in this article, I’d rather discuss how inflation is impacting investment markets currently. You will likely have noted subdued performance of your portfolios over 2022 and in the early parts of 2023.

In between my first draft of this article and it publishing, the investment landscape changed dramatically. The collapse of Silicon Valley Bank and the fall of Credit Suisse has dominated headlines and rightly so. It is likely I will address this in a separate article, but our message to clients has been that Australian banks are well capitalised and operate far more conservatively than those that are currently problematic. Governments and central banks have stepped in to ensure that depositor’s funds remain safe, and as such there is unlikely to be a “run on banks”. At it’s core, it is the dramatic increase in interest rates that has caused these bank’s downfall. This may see a brief pause to the tightening cycle.

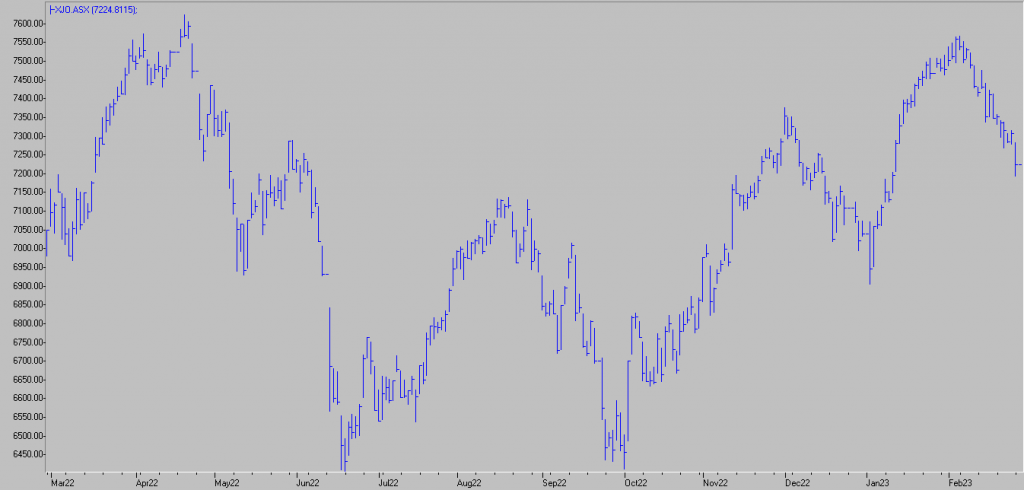

The Australian sharemarket over the last 12 months has been volatile, and largely gone nowhere! Early year high points were quickly forgotten as markets fell quickly once the RBA started increasing rates. Once investors became comfortable with the rate rises, a significant rally ensued during late 2022. In January 2023, the ASX200 jumped 6.2%, marking it’s best January ever! However, in February and March, we gave most of the gains back.

February is “Earnings Season” for ASX-listed companies. One by one, they announce their half yearly results. These result rarely move the overall market – the overall market is driven more by macroeconomic factors, however they provide interesting observations. Record profits have been announced by many companies, with Commonwealth Bank and Qantas the stand-outs. However, their share prices were subsequently smashed. Other companies (such as Dominos Pizza) had poorer results, and their share prices were decimated too. Good results equalled share price weakness, poor results too equalled the same! The reason is less to do with past results, and more about their outlooks. CBA, Qantas and many highly profitable companies expressed reservations about their next 6 to 12 months. Most of their concern linked back to inflation and the impact of rising interest rates. For Qantas, it is reasonably obvious – if the consumer has less funds for discretionary spending, travel will suffer. For the banks, while rising interest rates provide an opportunity for increased margins, the concern of debt/mortgage defaults is increasing.

We invest for the longer term for our clients, so the short term results and outlooks rarely sway our investment recommendations. Companies with long term track records of profitability, stable management, strong balance sheets and sustainable dividends can be afforded the odd bad result.

The current inflationary environment is part of the broader economic cycle, and will pass eventually. There are already small signs of improvement. Cash and fixed interest investments, which are a core part of most of our portfolios, are finally contributing to overall performance, and high quality shares and property investments should outperform smaller, more speculative companies during uncertain times.

Every stage of the investment cycle brings with it new uncertainty for the investor. They also throw up opportunities. Speak to one of our advisers today to discuss how your investments can navigate current conditions.