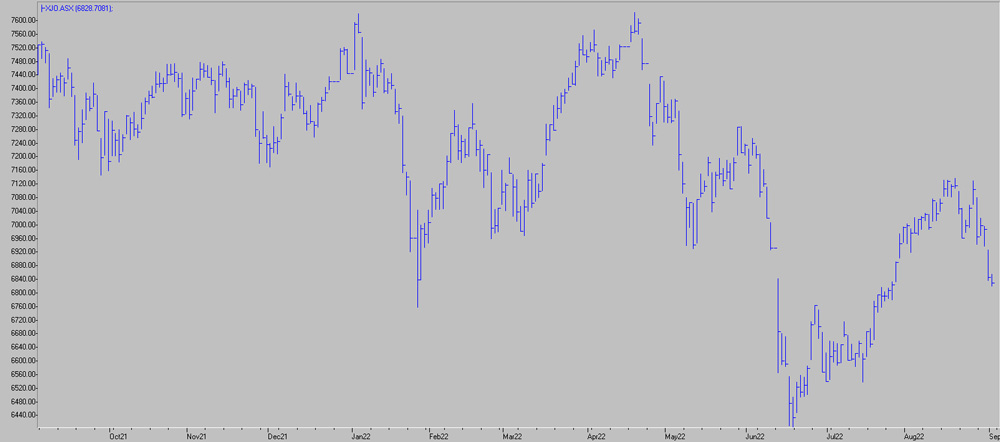

The last quarter saw large interest rate rises each month, with the RBA increasing the cash rate by 0.5% in each of June, July and August. The sharemarket reacted accordingly (well, at least initially!).

A sharp correction in June can be attributed to the first of the larger rate rises (while the RBA also raised rates in May, it was by a token 0.25%). The ASX200 then spent much of July and August recovering, before ending the quarter just over 3% down. The ABS announced an annual inflation (CPI) rate in late July of 6.1%, the largest annual rise since the ABS started producing the figures. This was not unexpected, but provided support to likely future rate rises throughout the remainder of 2022.

Unfortunately, the damage done in June meant that many financial year-end superannuation and investment statements look pretty ordinary as June alone wiped out much of the year’s reasonable sharemarket returns. Coupled with a horrible year for bond returns, the average ‘balanced’ portfolio showed flat or slightly negative returns for the 2021/2022 financial year.

ASX200 – Last 12 Months

Much of the recovery can be attributed to a better-than-expected reporting season. Reporting season overall was benign, but continued to provide evidence that the Australian economy, overall, is in pretty good shape. Temporarily at least, talk of a recession in Australia seems to have reduced. Much of the fall in the last couple of weeks can be attributed to the likelihood of the US entering a recession and a fresh COVID lockdown in China impacting our mining company share prices.

A valid question is – are the rate rises working as intended? That is, are they effectively lowering our inflation rate/cost of living. It’s probably too early to tell. There are some signs, particularly in the property market, that increased interest rates are biting. However, interestingly, there is no sign that rate rises are impacting retail consumer spending. Big TVs, lounge suites and computers are still flying out the door of retailers, and the demand for cars continues unabated. After a couple of years of lockdowns and restrictions, and record levels of household savings, pent up demand continues.

The RBA are watching all of this closely. They will no doubt be happy with the cooling of the property market, but with retail spending making up such a large percentage of the CPI basket of goods, the rate rises are likely to continue for some months yet. Rate rises and a lack of clarity about the effectiveness of them, as well as continued uncertainty in the biggest economies in the world (US and China) are likely to weigh on our sharemarket performance over the next quarter.