Some rules never change and the fundamental rule for long term investors is the power of compound returns.

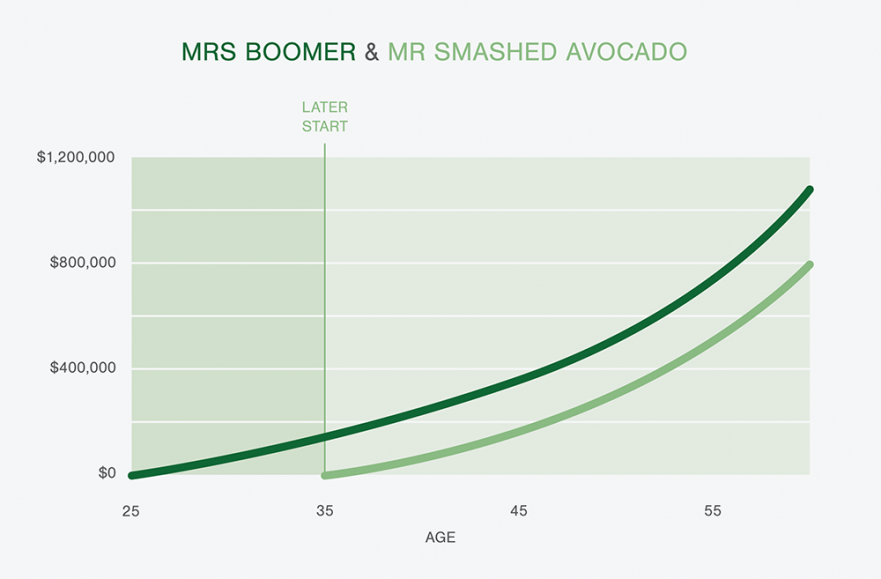

The above graph compares two investors, Mrs Boomer and Mr Smashed Avocado.

Mrs Boomer invests $10,000 per year between the ages of 25 and 35, then stops. Mr Smashed Avocado starts his investment at age 35 and contributes $10,000 per year all the way through to age 60. Both investments earn 8%. Who will have the larger balance at age 60?

Most people might assume the obvious answer is Mr Smashed Avocado because he contributed $10,000 per year for 25 years, a total of $250,000. That is more than double the amount invested by Mrs Boomer who only contributed a total of $100,000. But the graph above tells us otherwise.

Mrs Boomer has significantly more in her investment at age 60. That is because she started 10 years earlier and even though she contributes a lot less, she has the advantage of an extra 10 years of compound returns. This is because she is benefitting from a greater “time in the market”.

For someone in their 20s, putting money into super or other investments might not seem like a particularly attractive option. As the Mrs Boomer example vividly illustrates, investing from an early age can pay dividends over the long term.

Cash is probably no longer a suitable investment option for you or your family. Contact Wakefield Partners today to discuss alternatives.